CloudBankin’s Credit Decision Engine Software

Quick decisioning engine. Configure parameters, underwrite borrowers. Credit decisions in 2 minutes.

Accelerate Your Decision Making. Automate Your Lending Process.

Ensure the best outcomes based on your needs. Our rule engine as a service, which helps the loan origination system, configures all the business rules and credit parameters based on your credit policy. With a flexible and easy-to-use credit risk engine, we help empower your business, accelerate decision-making, and automate your lending process.

Takes Only 2 Minutes To Make A Credit Decision!

CloudBankin’s rule engine software is configured with the rules that make the credit policy. Data of the borrowers obtained from sources like Aadhar, PAN, CKYC, Credit Bureau, Bank statement Analyser, Alternate data, etc., are used as data points in the rule engine. The rules associated with these parameters are easily configurable. We have configured 2000 data points and can add more based on your requirements. Manual intervention can be minimised to the extent of taking informed final decisions when necessitated. Get the Credit Assessment Memo as the output.

Set your parameters easily, let our decision engine evaluate your borrowers and make credit decisions within minutes based on the outcomes with our inbuilt analytics!

Configurable Based On Your Conditions

Integrate Inputs From APIs Easily

Make Decision Making Quicker And Faster

Make Underwriting Process Automated

Reduce Underwriting Process Time

Implement Any Number Of Changes

Error Free

Easily Customise Loan Offers To Borrowers

Automate Credit Decision & Manual Intervention (If Needed)

Loan Approval Within Minutes

Give Loan Offers To NTC Borrowers Easily

No Code Platform

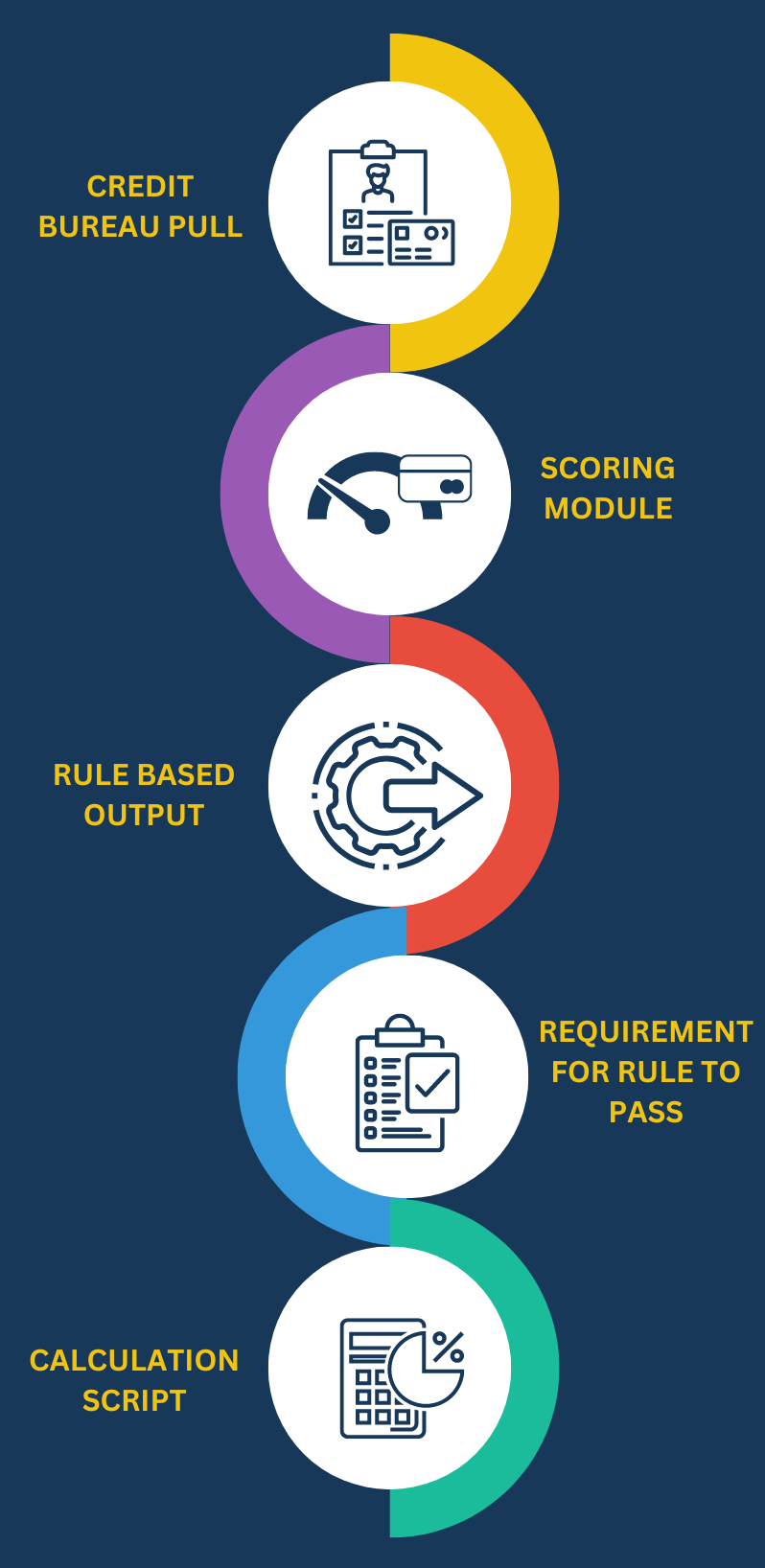

Our Rule Engine Modules

1. Credit Rule Assessment Criteria Module

This module in our rule engine software is set up based on your credit rules that check for the eligibility criteria for the borrowers. Two types are integrated here:

-

Soft Credit Pull

A preliminary credit check appears on a credit report just like any other inquiry. Whether your borrower checks his own credit report or you are periodically reviewing his current credit accounts, a soft check is conducted. The soft inquiry doesn’t affect the credit score and can happen even if your borrower hasn’t applied for credit.

-

Hard Credit Pull

Your borrower gives you consent to check his credit report, which you need for the final decisioning. This is when a hard check occurs. This might even affect the borrower’s credit score.

2. Scoring Module

You can configure a basic score for each condition in the rule engine. The system will automatically create the borrower’s scorecard. For example, if your credit score is higher than 600, you should give a score of 10; if it’s higher than 650, you should give a score of 12. In this way, set scores for each condition and then produce a scorecard for the borrower.

3. Rule-Based Output

Our rule engine software will provide you with the results so you can make a credit decision after evaluating and processing your borrower’s loan against different conditions like age, credit score, borrower’s current salary, any prior loans of the borrowers, interest rates, and 100+ parameters. For instance, If a credit score is greater than 600, the interest rate is set at 12%, and if it is lower than 600, the interest rate is raised to 15%.

4. Requirement for Rule to Pass

We will be able to specify fundamental eligibility requirements in our rule engine, on the basis of which it will choose whether to accept or reject the borrower. For example, the minimum age requirement is 18. If the borrower is over 18, the application will be accepted; if they are under 18, the application will be rejected.

5. Calculation Script

Set up and manage your calculations based on various parameters of the rule engine platform. For example, we calculate Debt-to-Income Ratio and other financial ratios without touching the code.

Our Rule Engine Processes

Our credit risk engine software supports two processes. Whichever you need, we have it.

Straight Through Process

This involves complete automation where you directly view your borrower’s eligibility result with a loan offer after processing.

Underwriter Process

Here, our risk engine software shows borrower’s eligibility outcome to the underwriter after processing. Underwriters can verify and manually choose to give loan offers corroborating the engine’s result.

Ready to explore our business rule engine?

Get the best business results with our automated, flexible, customizable decision-making software!

Frequently Asked Questions

What is credit decisioning engine software?

A credit decision software or a credit rule engine software is a customisable platform that is automated based on lenders' credit policies and rules and gives out the results to make credit decisions within minutes. It is designed for Banks, NBFCs and other financial institutions to make easy and quick credit decisions and manually save time for their underwriting process.

How long does it take to make a credit decision using CloudBankin’s decision engine software?

Using our rule engine software, you can able to make credit decisions within 2 minutes.

What are the modules of CloudBankin’s rule engine platform?

1. Scoring Module - It is used to assign scores to each requirement and then generate a scorecard for the borrower. 2. Rule-Based Output - After analysing and processing your borrower's loan in light of 100+ parameters, it will give you the results so you can decide whether to extend credits to your borrowers. 3. Requirement for Rule to Pass - It will determine whether to accept or reject a borrower based on its specific and fundamental eligibility requirements. 4. Calculation Script - You can manage and set up your calculations, like DBR and other financial ratios, based on different parameters.

How many data points does it support?

Our software is set up with more than 500 data points. Depending on your needs and requirements, we can even add more.

What are the processes of CloudBankin’s decision engine software supports?

Our rule engine software supports: 1. Straight Through Process - It is entirely automated, and you can see borrower eligibility outcomes directly. 2. Underwriter Process - It displays results for borrower eligibility to the underwriters, who can manually confirm and decide whether to make loan offers that support the engine's outcomes.

Is the rule engine configurable?

Yes, it is configurable. 1. You have the option to add/modify/delete a rule engine’s parameter. For instance, you may have chosen to accept a borrower if there are 3 active loans, rejecting them otherwise, if more. However, you want to lower the value to 2. Without a doubt, you can change it. It is that configurable. 2. In order to thoroughly assess your borrowers, you may want to add a new parameter. For instance, you can add additional information about your borrowers, such as their GPS location or their online activity, to evaluate them more thoroughly. 3. Another instance is that you have obtained data from the credit bureau, but now you want to perform your own calculations to evaluate your borrowers. You can do any number of calculations using our calculation script module without any development effort.

What variables or parameters do we add to the rule engine?

We get data from sources such as: 1. KYC, 2. Credit Bureau, 3. Bank Statements, and 4. Alternate data like SMS transactions. We take these variables as inputs and then produce a borrower scorecard that enables lenders to make credit decisions more quickly.

Related Articles

- Email: salesteam@cloudbankin.com

- Sales Enquiries: +91 9080996606

- HR Enquiries: +91 9080996576

After smartphone penetration, people are not watching their SMS at all. They use SMS only for OTP related transactions. That’s it.

But What can a Lender see in your SMS after you consent to them?

Lender can see income, expenses, and any other Fixed Obligation like (EMIs/Credit Card).

1) Income – Parameters like Average Salary Credited, Stable Monthly inflows like Rent

2) Expenses – Average monthly debit card transactions, UPI Transactions, Monthly ATM Withdrawal Amount etc

3) Fixed Obligations – Loan payments have been made for the past few months, Credit card transactions.

It also tells the Lender the adverse incidents like

1) Missed Loan payments

2) Cheque bounces

3) Missed Bill Payments like EB, LPG gas bills.

4) POS transaction declines due to insufficient funds.

A massive chunk of data is available in our SMS (more than 700 data points), which helps Lender to make a credit decision.

#lendtech #fintech #manispeaksmoney