In today’s competitive market, people are lacking behind in time to complete their routine. Hence, it is important to have time-saving technology in places wherever possible – be it a loan processing system or anything that is similar.

Manual processing in financial and banking sectors often results in delayed processing. Especially, when it comes to loan management system – handling huge amount of data will slow down the entire process.

The best way to eliminate all the issues in the loan processing system is to automate it. Cloud-based loan management software speed-ups the entire process and eliminates the overheads. It helps to streamline, manage, and automate the entire loan processing system.

Read further to know more about the cloud-based loan management software…

Automated Loan-Processing System

The cloud computing technology has transformed the lending industry as well and now, lenders and borrowers are getting benefited from it. Now that the cloud-based loan processing system has come into existence and this has transformed the process to a whole new level.

Ranging from loan origination to loan servicing, cloud computing is making these services available to a broad range of clients.

This has simplified the entire process and has created the following impacts:

● Lowers the overall processing cost

● Enhanced productivity

● Increased profitability

● Eliminates the need for paperwork

● Better customer satisfaction

● Easy to process a large number of loan applications

Automation of loan processing system creates a positive impact for both the lenders as well as the borrowers. It provides a better experience for the customers by making the process simple. Also, this has streamlined the loan process and helps to meet business goals.

Cloud-based loan management platform is a boon to financial organizations and eases out the entire process. The major advantage of this platform is that it helps you to manage a large number of data sets efficiently without costing you much money.

Read further to know about the basics of the cloud-based loan processing system and its benefits…

Cloud-Based Loan Processing System

With every in business going digital, cloud platforms have become prominent and play an essential role in all the business sectors. The financial sector is no exception. In fact, cloud-based solutions are transforming the finance sector with a new perspective and solutions.

Use of cloud-based solutions has resulted in better management of the lending process and involves less paperwork. Also, the entire process from loan origination to loan servicing is completely streamlined. Cloud-based loan processing system is a way more secure than the manual system and offers extra security to the users/customers.

The customer support services are extended for 24/7 and thus, this adds an entirely new dimension to the concept. With the use of cloud-based loan processing system, banking and financial organizations can surely gain an edge over their major competitors. This also helps organizations to bring in dynamic work culture in the marketplace.

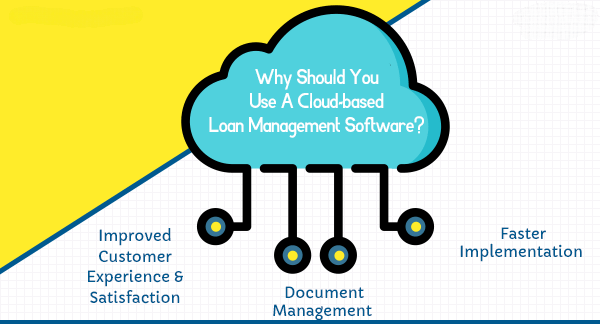

Benefits of Using Cloud-Based Loan Processing System

Cloud computing technology has the potential to transform the financial services business by completely reinventing the business model. It helps lending organizations to connect easily with their customers. At the same time, business needs are met in a shorter time within a limited budget.

This makes lending organizations focus on their business innovation, thereby building greater customer experience.

Here is the list of key facts that highlight the benefits of cloud-based loan processing system:

Improved Customer Experience & Satisfaction

A manual or traditional loan processing system is time-consuming and requires a lot of manpower. Cloud-based loan processing system helps you to overcome all these issues and reduces the overall processing time.

In a manual-processing system, lenders usually charge a higher processing fee, but when using a cloud-based system, all these overheads and other costs can be cut-off eventually. Moreover, with the cloud, you can offer more and more services to your customers across multiple channels.

The overall processing time, paperwork, error-rate, and other issues including a huge amount of manpower, workplace, etc can be reduced. Lenders need not spend long-time for completing the process and can easily get their loan amount.